News & Insights / AnBro Q2 2026 Update: Chaos and Consequences

AnBro Q2 2026 Update: Chaos and Consequences

AnBro's Q2 2026 market update explores the global events shaping financial markets, from geopolitical tensions and inflation to the continued rise of AI investing. Read AnBro CIO Craig Antonie's latest market outlook and portfolio performance review for TITANS, Dynamic Compound, BRNDZ and UNICRN.

- July 9, 2026

- by Mesh

What a ride 2026 continues to be, nobody can accuse us of living in a boring world, especially with so many narratives fighting for airtime concurrently. Depending on your point of focus you’d have the ongoing issues in the middle east pulling against the AI trade which also might side track you away from the UK losing another Prime Minister and the changes at the head of the Federal reserve! Surging global protectionism, sovereign debt strain and the US midterms due later this year will keep us engaged.

Thankfully, on the geopolitical front things have reached a semblance of calm, for the time being anyway. The war in Iran seems to be over. Most parties look keen on moving on from here. Cynics the world over will ask what was accomplished by all of this, and on the surface anyway I’d have to agree with those suggesting very little. Roughly 125 days into the conflict we have an ‘MOU’ but no deal yet. Oil prices have almost roundtripped their move back down, Iran still refuses to give up its Uranium and all we have is what seems like a lot of regional damage and global economic chaos, the consequences of which are still being felt in varying ways. Some countries have had to scramble to make sure they can keep the ‘lights on’, others have warned about fertilizer shortages which may impact crops (el Nino’s not helping either), relationships between allies have been strained and of course supply chain strain and bottle necks have increased the cost of almost everything.

Inflation and stagflation fears have re-emerged which has had a profound impact on the outlook for interest rates. In some cases, cuts or the hope of them have flipped to actual rate increases (South Africa and the Eurozone) whilst the tone has shifted materially in others (USA, UK, Canada and Australia). With oil shifting lower perhaps inflation anxiety will ease but we need to see oil flowing and infrastructure being repaired to be comfortable it sticks.

I’ve always tried to steer away from politics; it sits in the ‘too hard’ basket for me. It’s one of the only areas I’ve ever come across where logic and sanity cross paths and somehow the result seems to be illogical and insane. So, for the sake of our own mental wellbeing, we won’t spend too much time on the UK other than mentioning what seems to be a clear trend (globally) that people are becoming increasingly frustrated with how things are being done and the way they are being managed. It’s certainly something we need to keep an eye on, especially in the US where a high stakes game has been played ahead of Midterms due to take place on the 3rd of November. We can expect a lot of jawboning and some volatility as we get closer to the event.

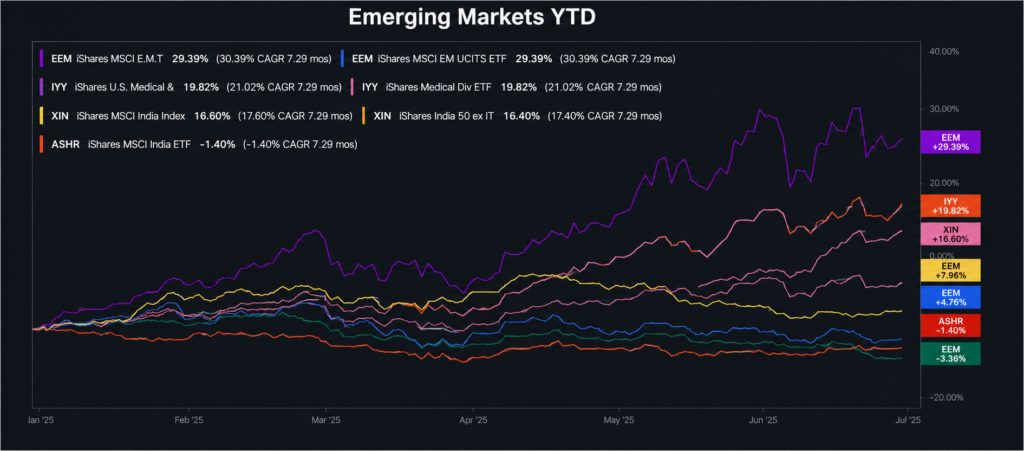

From a market’s perspective, it’s been another strange year so far. Once again, on the surface, we’re at a place of relative calm, indices around the world have steadied and, overall, look a lot better now than earlier in year. Underneath the surface it’s another story. Emerging markets as a basket have risen sharply but, in most part, because of a massive rally in South Korea and Taiwan (and specifically, due to just a handful of shares, Samsung Electronics, SK Hynix and Taiwan Semi). China, India and SA on the other hand have lagged. This is the AI trade in full force.

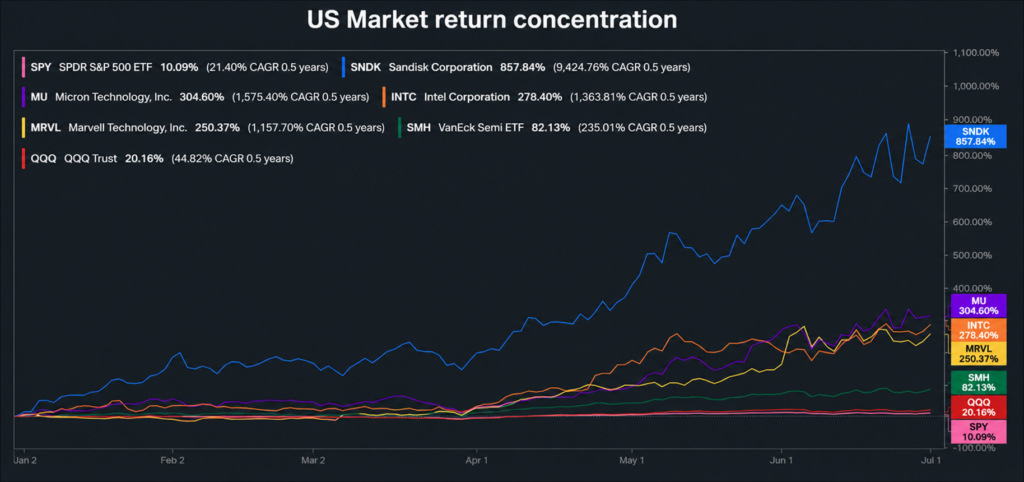

In the US it’s even more confusing. The standout sector has once again been Information Technology BUT the performance isn’t coming from the large caps. Microsoft is down 23% this year, followed by META which is 15% lower. Amazon, Apple and Nvidia have squeezed out a gain of about 5% on average. Alphabet is the only Mag 7 stock ahead of the market at 12%. It’s literally been a mammoth rally of semiconductor and memory companies which have almost single handedly pulled the whole market higher this year. The sheer returns from names like Micron, Sandisk, Intel & Marvell alone have added about 2.5% to the S&P500 and 6% to the Nasdaq. The Semi-Conductor sector as a whole is up a whopping 82% this year. It has almost single handedly driven market returns in 2026 to date. At the half year the market is up about 10%. Semis are worth 6% of that gain. Similarly, the Nasdaq 100 is up 20% with Semis accounting for about 15% of the move.

The massive AI rally we’re seeing in 2026 continues to plaster over the broader implications of tariffs, the oil price shock and a continuing slow decline in the US jobs market. This continues a trend where the last several years has seen one dominant trend drive returns.

2023–2024: The “Magnificent Seven” Era

Started out at the birth of AI as an investment theme. The focus was on generative AI and Software platforms. Investors poured money into a small cohort of mega cap companies which became known as the Magnificent Seven. Microsoft, Nvidia, Apple, Alphabet, Amazon, Meta, and Tesla.

2025: The Hyperscaler Expansion

In 2025 the theme shifted to massive cloud provider capital expenditure. The largest technology companies accounted for over 53% of the S&P 500’s total return for the year, as Wall Street cheered the hundreds of billions of dollars being committed to building the AI grid.

2026: The Semiconductor & Hardware Bottleneck

We’ve seen a narrowing into the physical “plumbing” of AI, specifically, semiconductors and highbandwidth memory. Semiconductor companies now represent nearly one-fifth (20%) of the entire S&P500; the highest industry share ever recorded.

It’s been a sight to behold and quite incredible. At the same time however, from a risk perspective, diversified portfolios continue to deliver acceptable returns with far less volatility. I suspect that the time for diversification is getting ever nearer as investors begin to fret about the massive cash spent and debt incurred on these three trends covered above. Risks certainly seem to be building as the one ‘big trade’ is slowly showing signs of fracture. Balance sheet strain, cash flow consumption, bottle necks and pricing are forming a formidable push back to the momentum we’ve seen here to date.

AnBro Portfolios Performance Highlights

Core Portfolio

The AnBro TITANS Core portfolio continues to do what it says on the box. YTD in USD the portfolio has returned 7.23%. This blue-chip, high-quality, well diversified portfolio has done this in a better risk adjusted fashion and with lower volatility than the broader market.

TITANS Biggest and Best – Titans

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Industrials | GE Vernova | Constellation Energy | Utilities |

Industrials | Caterpillar | Microsoft | Information Tech |

Real Estate | Equinix | Netflix | Communication Services |

Health Care | United Health | Booking Holdings | Consumer Discretionary |

Materials | Linde Plc | CRH plc | Materials |

This core portfolio should be compared to the S&P500 from both a returns and RISK perspective over the LONG TERM. Any investor that invests in, or has considered, an S&P500 tracker fund for their core holding could do well by considering the TITANS portfolio instead. (The AnBro Unit Trust ANGGFB was changed to this mandate in May of 2025). This portfolio is also available in Frankfurt under ISIN: CH1441034159

Conservative/Balanced

The AnBro Dynamic Compound Portfolio ended the half year with a gain of 7.45%. Its overall defensive posture has delivered solid growth alongside growing cash flows. Dividend growth of 8% and a current yield of 3.42% has allowed for a continual source of cash flow from which we can reinvest into opportunities as they present themselves. The sharp rebound in the AI trade in the quarter allowed us to harvest some profits in our positions in Dell and Cisco. This cash and some dividends were then used to invest in new positions in a handful of US utility stocks, most notably Entergy, NiSource and NRG Energy. We also used dividend accruals to take advantage of a slump in some wonderful long-term compounders that have been sold during all the semiconductor exuberance. Rollins, HCA Healthcare and Halma plc were such examples that have been topped up on weakness. The top and bottom five performers in the portfolio YTD are:

Tracking back to when the world went haywire (for me personally this was the onset of lockdowns and COVID19) the TITANS returns have been exemplary.

Dynamic Compounding – ANCOMP

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Information Tech | Dell | Boston Scientific | Health Care |

Information Tech | Cisco | Rollins | Industrials |

Health Care | CVS | Abbott Labs | Health Care |

Real Estate | Equinix | Reckitt Benckiser | Consumer Staple |

Financials | Hiscox | CME Group | Financials |

As a reminder this portfolio is positioned as a defensive investment. We expect less volatility in a risk off market and consider it as the more conservative of the strategies we run. It is also available in Frankfurt under ISIN: CH1231066734

High Quality/Diversified

The AnBro World’s Biggest Brands Portfolio rebounded from Q1 declines and is currently up 1% year to date. The biggest brands in the world include a healthy dollop of MAG7 companies and as alluded to above the market has been lukewarm on most of them this year. Current large weights in Alphabet and Apple have helped offset declines in Microsoft and META. Similarly stand out returns from Intel, Dell and Samsung have offset a decline in software stocks and those perceived as under threat from AI such as Accenture, Salesforce and Adobe. As a reminder we model for the world’s 100 largest brands and then weight the portfolio according to BRAND VALUE. Those brands with the highest value get a higher allocation of capital.

World’s Biggest BRNDZ – BRNDZ

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Information Tech | Intel | Intuit | Information Tech |

Information Tech | Dell | Accenture | Information Tech |

Information Tech | AMD | Xiaomi Corp | Information Tech |

Information Tech | Samsung | Salesforce | Information Tech |

Information Tech | Texas Instruments | Adobe | Information Tech |

This is considered a high quality, diversified, global portfolio by the team at AnBro. It is a thematic portfolio that tracks consumer preferences on a worldwide basis and is ‘on trend’ for the global consumption evolution. It is also available in Frankfurt under ISIN: CH1332120158

High Growth/Blue Sky

Higher growth, higher BETA stocks bounced in the second quarter and the Unicorn portfolio (JSE: UNICRN) jumped 15.2% over the period in USD. This portfolio is looking to benefit from the AI trade but not in the obvious sense. We do have semiconductor and Hyperscaler exposure, but the bulk of the strategy remains to those businesses that are benefitting and using AI versus those that are simply enabling it. It is looking at the shift in AI from a ‘conceptual’ to an ‘operational’ perspective. Over and above this, the continuing trend in decarbonisation off the back of surging energy demand is worth monitoring.

Three themes: AI, Energy Independence and Energy Transition are converging and creating vast opportunities as companies strive to be more efficient. This is also incorporated into the current portfolio allocation. The globe seems steadfast in searching for ways to reduce reliance on the Middle East and Russia as the second energy shock in 3 years collides with a ramp in energy demand courtesy of AI energy intensity, the continued adoption of EV’s and a build out and refresh of existing grid infrastructure.

UNICORN – UNICRN

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Information Tech | Dell | Constellation Energy | Utilities |

Industrials | Bloom Energy | SunRun | Industrials |

Information Tech | Corning Inc | Microsoft | Information Tech |

Information Tech | Allegro Microsystems | MercadoLibre | Consumer Discretionary |

Industrials | Vertiv Holdings | First Solar | Information Tech |

The AnBro Team see this portfolio as the one that offers the highest growth and blue-sky potential. It suits long term investors looking to buy a piece of companies that offer massive long-term upside. It is by far the most ‘exciting’ portfolio we run and certainly the most volatile too. It is also available in Frankfurt under ISIN: CH1231066445

Closing Thoughts

As we enter the second half of the year, there remains a lot to be aware of and excited about. The AnBro portfolios allow clients to express their views of the world in multiple ways and we’re happy with their respective individual positioning and the opportunities they provide for long term investors. Please get in touch if you’d like to chat about or have any questions regarding the investment suite.

Chat soon,

Craig and the AnBro team.

Tags

27Four Alternative investments AltFi Bankruptcy-remote Blockchain Capital Markets Capital Markets of the Future Commodity Markets Copper investment Crypto Markets DeFi Financial Markets Fully backed stablecoin Global Markets Gold Industrial Metals Investing Investment Liquidity management Mesh Mesh Mint mZAR Open to all Regulation Secondary Market Smart Assets Stablecoin transparency Tokenisation Tokenised cash Yield-bearing stablecoin yZAR

- AI Investing, AnBro, BRNDZ, Dynamic Compound, Equities, Global Markets, Offshore Investing, Portfolio Performance, Quarterly Update, TITANS, UNICRN

Want to stay in the know on upcoming events and seminars?

Newsletter Sign Up

For more press information, please contact:

Connie Bloem, Product owner of Mesh:

hello@meshtrade.co / +1 604 671 4515