News & Insights / Q1 2026: From Record Highs to Oil shock – Our Core slept well at night

Q1 2026: From Record Highs to Oil shock – Our Core slept well at night

Chief Investment Officer Craig Antonie examines the performance of the different Λnßro portfolios in the first quarter of 2026.

- April 16, 2026

- by Mesh

Market Review

Coming into 2026 markets were keeping an eye on global economies with a sense of relative calm. The US was still expected to deliver solid growth this year helped by the massive deployment of Capital into the AI space. Inflation was under control and trending lower. The weaker USD was boosting commodity prices, emerging markets & currencies and Europe was continuing to attract strong global inflows as lower valuations, lower interest rates and a lift in fiscal spending made investing there more attractive. The S&P 500 hit a record high early on, as did the JSE All Share index. The DAX, CAC40, FTSE100, KOSPI and Nikkei were also on a long list of record-breaking indices. This despite ongoing Tariff threats, the spat over Greenland and the changes in Venezuela.

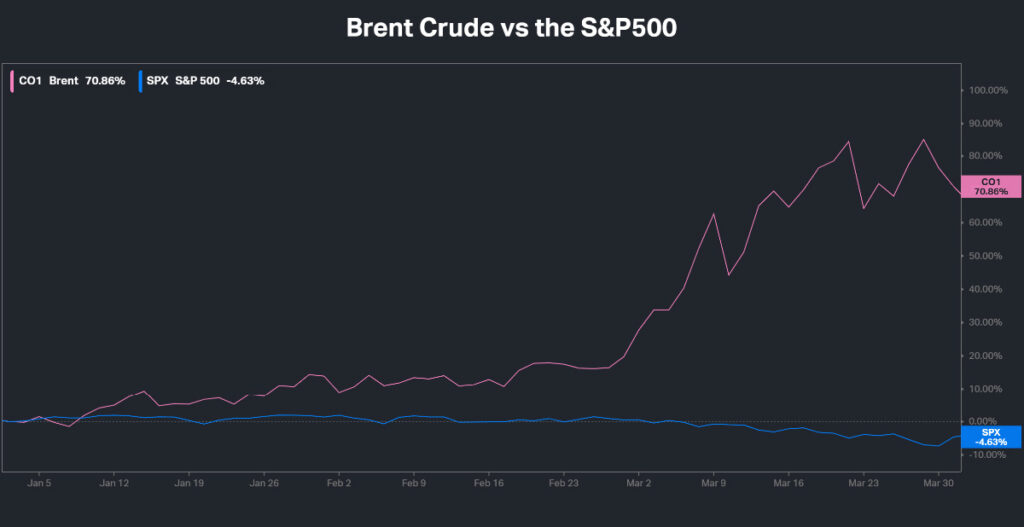

We know what happened next right. Strong market breadth and record setting gains gave way to volatility and a draw down across the globe as the war in Iran took hold. Oil prices soared with the war removing roughly 20% of global energy flows from the market as the Strait of Hormuz was effectively shut. Brent crude started the year at around $61 a barrel it then soared to just shy of $120 at its peak before settling at $104 by quarter end.

The markets’ reaction function was quite swift as you would imagine. Inflation expectations shot upward, the USD strengthened, commodity prices fell, bonds sank lower and supply chain pressures for multiple industries triggered risk off sentiment. When it was all said and done some sharp reversals had taken place. At the end of the quarter the S&P500 is down 4.63% for the year. The JSE All Share was marginally weaker at -1.2% (in ZAR), with multiple markets dropping 10% or more from their highs and effectively entering ‘correction’ territory.

The importance of a strong CORE – AnBro TITANS Performance

A lot of ink is being spilled on where we go from here. At the time of writing markets are bouncing off recent lows on the hopes that a resolution to the conflict is imminent. We all hope this the case as a world full of wars serves nobody positively. From a Macro perspective we are yet to see the full impact of this.

Markets are rapidly ping-ponging around on daily tweets and headlines and as long-term investors we know a level head is needed alongside the ability to withstand the whipsawing we are likely to see to come out stronger at the end of this. For now, we do not know what the outcome is and what the ramifications of these actions will be on economies, inflation, interest rates, oil prices, fertilizer prices, and food prices (to name a few). The second and third order impacts are difficult to quantify as they change depending on your view on IF we get a resolution or not, on the duration of the conflict and on what the conclusion looks like.

It is a reasonable assumption (I think) that its likely energy markets have changed for the longer term. Countries originally worried about tariff pressure now need to rethink their energy security too. Who do you align yourself with to ensure disruptions like this don’t occur in future (there have been too many dislocations in supply chains and energy supply since COVID19). Do countries or regions try to secure their own sources of energy? Do we see a step up in energy independence agendas from governments?

We don’t know yet how it pans out but what we do know is ultimately the world ‘figures it out.’ It is especially during times like this that we want to be able to sleep well at night and in this vein, I would like to spend a couple of minutes on the AnBro TITANS portfolio. This is our CORE portfolio and is aimed at investors looking for better risk adjusted returns than the S&P 500. This is our most widely held portfolio and so in times of crisis its worth discussing.

The AnBro TITANS portfolio was built to give investors that invest in or track the S&P500 ‘a better alternative’ to the major index. It focuses on the 11 GICS sectors that make up the US market and homes in on the best companies we can find in each sector. Using our proprietary models we search for top tier companies that tick many boxes such as, management, quality, liquidity, size, balance sheet strength, margins, track record, growth outlook and more in order to build a portfolio we think is ultimately as bullet proof as one can be (vs the S&P 500) for various economic cycles and circumstances. Its diversity is its strength, and its quality is where we aim to generate long term Alpha from.

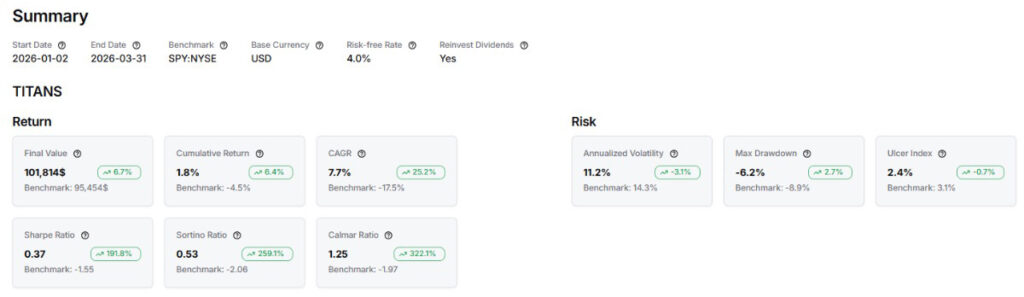

As at the close of business on the 31st of March 2026 the AnBro TITANS portfolio was up 2.11% in USD compared to the decline in the S&P 500 of 4.63%. The relative return vs the market is a very healthy 6.74%. Returns are widely dispersed as one would expect in a portfolio this well diversified but splitting out the pieces, we can quantify it as follows:

Energy is the standard out winner so far YTD with gains of 35.7%, followed by Industrials at 11.4%, Consumer Staples 9.2%, Real Estate 8.4% & Materials 6.1%. Utilities and Healthcare were also in the green. The biggest laggards YTD come from Information Technology -12.4%, Communication services -10.7%, Financials -10% & Consumer Discretionary -9.55%.

Clearly Tech and financials have suffered the brunt of this market selloff, however it has been more than offset by gains elsewhere. I alluded to diversity as a key strength of this portfolio and it’s showing its value during this time. The fact that TITANS has no stock concentration risk, no sector concentration risk, is full of blue chips and companies that operate around the globe make it perfectly positioned to naturally pivot to whichever market or macro regime we find ourselves in.

Importantly this portfolio is reconstituted and equally weighted at the beginning of each year. The nuance here is critical because it allows us to drift with the macro and market driving forces as they happen. We then systematically take profit and reset annually and then drift again with the drivers of the moment. What this has demonstrated over time is that our draw downs (as evidenced by our SORTINO ratio) are far less extreme than the broader market which not only positions us better for when markets turn around (as we rebound from a higher base) but we also experience less volatility and with it much lower investor angst. The portfolio’s SHARPE ratio is also superior to that of the market too which then allows for the capture of upside in a less volatile way.

Drawing data from Portfolio Metrics the YTD figures look like this assuming an initial investment of $100 000.00 on 1 January 2026:

Similarly, it has a high correlation (84.5%) to the broader market but a much lower Beta, YTD its beta of 0.66 is demonstrating the lower volatility of the portfolio, which has not had a negative impact on returns.

Breaking it down by stock performance YTD the top five winners and losers look like this:

Titans

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Energy | ConocoPhillips | Microsoft | Information Tech |

Energy | Exxon Mobil | Take-Two Interactive | Communication Services |

Energy | EOG Resources | Booking Holdings | Consumer Discretionary |

Energy | Chevron | Constellation Energy | Utilities |

Industrials | GR Vernova | United Health Group | Health Care |

*YTD performance |

The top and bottom of the portfolio from a weighting perspective looked like this as we ended the first quarter of 2026.

Top 10 | Bottom 10 |

|---|---|

ConocoPhillips | Eii Lilly & Co |

Exxon Mobil Corporation | The Walt Disney Corporation |

EOG Resources Inc | CRH PLC |

Chevron Corp | Tesla Inc |

GE Vernova Inc | Palantir Technologies Inc |

Equinix Inc | United Health Group Inc |

Caterpillar Inc | Constellation Energy Corp |

The Williams Cos Inc | Take-Two Interactive Software Inc |

Johnson & Johnson | Microsoft Corp |

Linde PLC | Booking Holdings Inc |

Over the years, we have managed this portfolio as a segregated portfolio. It’s the CORE from where our satellite portfolios of Unicorn, AnComp & BRNDZ were born. The CORE provides each satellite with its foundational stocks, and the portfolios are then built out from there. TITANS therefore provides you with the anchors of each satellite rolled up into one uber blue chip package.

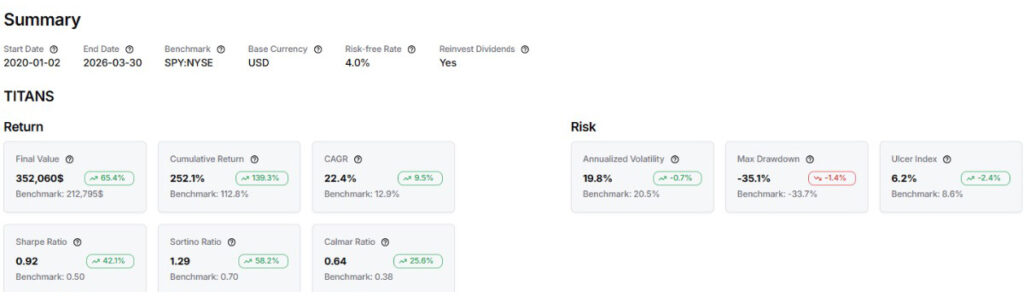

Tracking back to when the world went haywire (for me personally this was the onset of lockdowns and COVID19) the TITANS returns have been exemplary.

Over the longer term its correlation to the market is higher at 96.1% and the of Beta 0.93 is still lower than the S&P500. However, as you can see its SHARPE and SORTINO ratios are superior and combined they add up to market beating returns over time. This has happened despite quite a bumpy period including Covid lockdowns, two wars, a vicious interest rate and inflation cycle and two oil shocks.

Satellite Portfolio Update: AnBro Portfolios (Returns in USD)

Conservative/Balanced

The AnBro Dynamic Compound Portfolio (JSE: ANCOMP) ended Q1 2026 up 1.37%. Its overall defensive posture helped it endure the volatility of markets. Its relatively large weight in Europe did act as a drag post the outbreak of the war in the Middle East, but the quality of the underlying stocks meant we ‘suffered less.’

As is usually the case in the first quarter we start seeing dividend announcements for the new year and some standout increases came from the following investments: Hanover RE 39%, HCA Healthcare 18%, DELL 19%, Equinix 10%, NextEra Energy 10%, Abbott Healthcare 7%. A host of companies raised in the 4-6% range. The current dividend yield of the portfolio is 3.3%. The top and bottom five performers in the portfolio YTD are:

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Information tech | Dell | Boston Scientific | Health Care |

Industrials | BAE Systems | Abbott Labs | Health Care |

Energy | Exon Mobil | Reckitt Benckiser | Consumer Staples |

Real Estate | Equenix | United health Group | Health Care |

Utilities | RWE | Rollins | Industrials |

*YTD performance |

Take me to AnBro Dynamic Compound

As a reminder this portfolio is positioned as a defensive investment. We expect less volatility in a risk off market and consider it as the more conservative of the strategies we run. It is also available in Frankfurt under ISIN: CH1231066734

High Quality/Diversified

The AnBro World’s Biggest Brands Portfolios (JSE: BRNDZ) ended the quarter down by 9.99%. The skew to technology in the biggest brands lineup contributed to the negative performance. Large cap tech has had a soft start to the year as market rotation and skittishness around massive AI Capex budgets have dented sentiment. During the second quarter the portfolio models are rerun, and the portfolio is reweighted, rebalanced and changes made where necessary. As a reminder we model for the world’s 100 largest brands and then weight the portfolio according to BRAND VALUE. Those brands with the highest value get a higher allocation of capital.

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Information Tech | Samsung | Intuit | Information Tech |

Information Tech | Dell | DoorDash | Consumer Discretionary |

Energy | Exon Mobil | ServiceNow | Information Tech |

Information Tech | Intel | HDFC Bank | Financials |

Industrials | FedEx | Adobe | Information tech |

*YTD performance |

This is considered a high quality, diversified, global portfolio by the team at AnBro. It is a thematic portfolio that tracks consumer preferences on a worldwide basis and is ‘on trend’ for the global consumption evolution. It is also available in Frankfurt under ISIN: CH1332120158

High Growth/Blue Sky

The AnBro Unicorn Growth Portfolio (JSE: UNICRN) ended the quarter down by 10.08%. Higher growth, higher BETA stocks came under pressure as volatility increased over the quarter. Fears around AI disruption touched many parts of the market especially the software space which continued to be sold off aggressively into the new year. The portfolios large exposure to cybersecurity hurt, however this was offset to a degree by exposures in areas of clean energy and AI infrastructure buildout names. We are of the opinion that despite what’s happening in the world today, the race for AI domination will remain ongoing. The portfolio’s core exposures are titled to those companies expected to profit from the capital being deployed at such massive scale at the moment.

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Industrials | Nextpower Inc | Zscaler | Information Tech |

Industrials | GE Vernova | DoorDash | Consumerr |

Utilities | Grenergy | Shopify | Consumer Discretionary |

Industrials | Dell | Axon Enterprises | Utilities |

Utilities | Solaria | Solaria | Industrials |

*YTD performance |

The AnBro Team see this portfolio as the one that offers the highest growth and blue-sky potential. It suits long term investors looking to buy a piece of companies that offer massive long-term upside. It is by far the most ‘exciting’ portfolio we run and certainly the most volatile too. It is also available in Frankfurt under ISIN: CH1231066445

Closing Thoughts

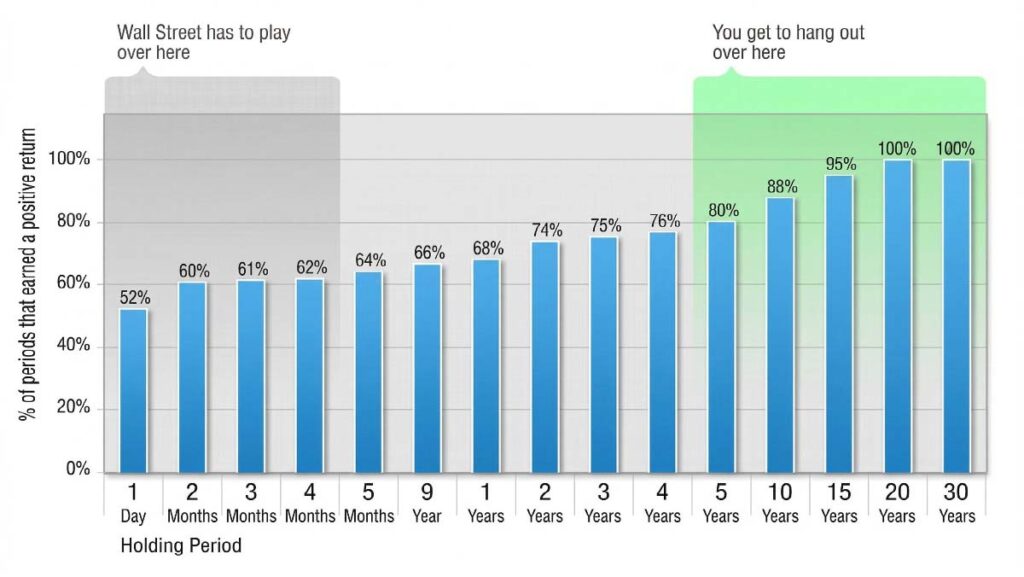

As we head into the second quarter of the year we once again find ourselves in a place where many unknowns exist. It is extremely easy to worry and stress during times of chaos and uncertainty, but long-term investors know this is par for the course and is not entirely unusual either in the world of investing. It’s always a good thing to remind ourselves that markets can and DO fall from time to time, but in the longer run your odds of winning rise exponentially. I’ll end of this quarters note with one of my favorite graphs.

Tags

Alternative investments AltFi Asset-Backed Finance Bankruptcy-remote Blockchain Capital Markets Capital Markets of the Future CCS Investment Platform Commodity Markets Crypto Markets DeFi Equipment Finance Financial Markets Fully backed stablecoin Global Markets Investing Investment Liquidity management Mesh Mesh Mint mZAR Open to all Regulation Secondary Market Smart Assets SME Finance Stablecoin transparency Tokenisation Tokenised cash Yield-bearing stablecoin yZAR

- Capital Markets, Capital Markets of the Future, Financial Markets, Global Markets, Investing, Mesh, Open to all

Want to stay in the know on upcoming events and seminars?

Newsletter Sign Up

For more press information, please contact:

Connie Bloem, Product owner of Mesh:

hello@meshtrade.co / +1 604 671 4515