News & Insights / Q3-25: One Step to the left

Q3-25: One Step to the left

In this excerpt from Λnßro Capital Investments’ quarterly newsletter, Chief Investment Officer Craig Antonie considers a steadier quarter and shifts shaping markets into year-end.

- October 14, 2025

- by Mesh

I can’t believe I’m saying this, but here we are entering the last quarter of 2025! Time just grinds by and if you blink, you’ll open your eyes and see the shops filling up with XMAS goodies (we’ve started seeing some of it here already in the UK, believe it or not!). I’m not quite ready for carols and reindeer just yet!

In my world, we keep marching on too! The last quarter was shaping up to be the calmest of the year so far and then suddenly it wasn’t.

The U.S.-China spat continues. Late last week, China imposed tighter controls on exports of rare earth elements and related materials essential for high-tech and defense industries to the U.S. This move came just ahead of the meeting between the two countries’ leaders at the APEC summit later in October.

Some viewed this as a bargaining tool ahead of the talks; however, U.S. President Donald Trump hit back hard in a social media post on Friday, threatening tariffs of 100% on Chinese products. The result was a significant market reaction on the day, with crypto markets, in particular, experiencing their worst liquidation ever. Some calm resumed over the weekend, however, as comments from both sides dialed back some of the initial fear. By Monday, markets had steadied; however, this is a sign that we shouldn’t be complacent, and the next few weeks are likely to remain eventful.

Markets have pretty much made ‘peace’ with the new US trade policy under President Trump. Deals were inked with major and minor parties and although some are still a work in progress, for the most part global exchanges have now stepped over this issue. After rebounding considerably from April lows, they continued higher and by the end of September, the US Market (as measured by the S&P 500) is up 13.72% year to date.

Looking at the last quarter company earnings results, things seem resilient considering all the headlines out there. Surprisingly, on a quarter-on-quarter basis fewer companies were citing ‘inflation’ and ‘uncertainty’ as potential headwinds according to FactSet. At the same time there are no obvious signs of broad-based deterioration in corporate earnings either, leaving many to believe that the Global economy and global markets by proxy have managed to dodge a pretty major bullet, that was a sudden shift in ‘cost structure’ post tariff implementation.

However, as we know there is always ‘the other side’ that we need to look at too, right. The steady decline in the strength of the US labour market has persisted and it was, in fact, these data points that resulted in what some have referred to as an ‘insurance cut’ by the Fed in September. Comments from the Fed Chair showed that even in the FOMC there wasn’t a clear consensus on how to correctly interpret events right now. These few stood out to me…

“It’s not incredibly obvious what Fed should do now”.

“officials’ diverse views unsurprising given complicated policy backdrop”.

“Job market indicators suggest meaningful downside risk”

Source: Chair Powell, Fed Press Conference, 17th September 2025

So, on the one hand corporate earnings and management commentary is fairly composed and even tempered, whilst on the other hand we have inflation that is still a problem, tariffs that, to be fair, still need a bit of time to filter into company bottom lines and a job market which is posing ‘meaningful downside risk’ as highlighted by Jerome Powell just a few weeks ago.

Markets have and are currently still focused on the positive side of this equation. The fact that we sit at or close to record highs tells us there is not a lot of fear or uncertainty out there, however, there clearly are some red flags as alluded to above.

With markets rallying so hard we have once again found ourselves at valuations which seem ahead of themselves, particularly if the job market in the US doesn’t find its footing relatively soon. Let’s not forget that the US economy is still driven in large part by consumer spending and the consumer is the jobs market!

Our sense is that a more cautious view is warranted for the next few months until the dust has settled and as a result, we have taken one step to the left in our portfolio allocation stance. What this means is that we’ve allocated our risk mandate a notch lower for the time being, with each portfolio adopting a tilt to more safety and lower Beta.

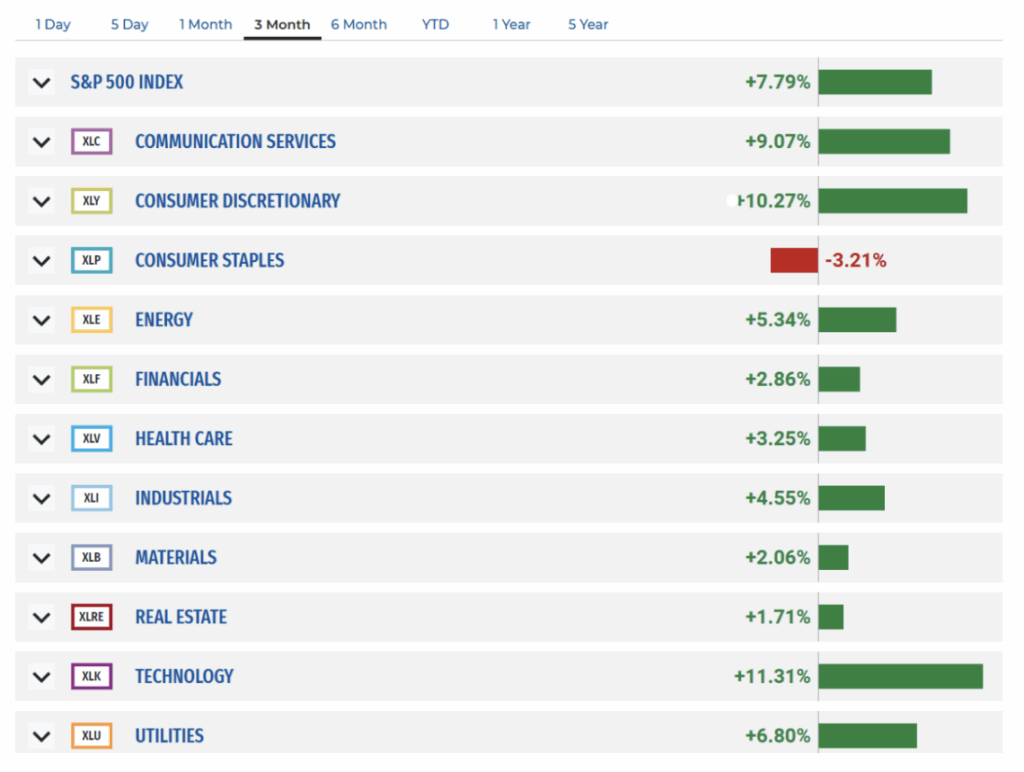

There are of course many sub trends that are driving market and investor behaviour right now and these can be quite easily observed by looking at quarterly sector returns. As markets recovered from early year losses and Q2 results showed resilience particularly in the large cap (Mag 7) space those companies continued to drive market returns. Appetite for defensive stocks once again waned as animal spirits chased growth and upside.

The market gained about 7.8% this quarter, but as you can see, it was just Communication Services (META, Alphabet) Consumer Discretionary (Amazon, Tesla) and the Technology sectors (Nvidia, Microsoft and Apple) that came in ahead of that.

On the other side, most other industries including, Consumer Staples, Health Care and Real Estate (the more defensive sectors) were quite a bit off the pace.

Looking Ahead

We raised market valuation as a question mark that was beginning to surface in our last note and after a further very strong quarter for the S&P500, that has become a greater potential headwind to future returns. As a result, as mentioned above, we have dialled back some of our exposure and have positioned our portfolios more conservatively for the quarter ahead.

Conservative/Balanced

The AnBro Dynamic Compound Portfolio (JSE: ANCOMP) ended the quarter up 1.9% and remains up 16.42% YTD. This portfolio is overweight global Insurance, Healthcare and Utilities and toward the end of the quarter we increased our exposure to the underperforming consumer staples sector. During market downturns or economic recessions, the companies that tend to perform best on a relative basis come from the latter three sectors. This portfolio now has a combined exposure of roughly 40% to these themes. A key feature of the portfolio, of course, is the dividend yield and dividend growth. The current yield is 3.2% and dividend growth year to date has been over 6%.

As a reminder, this portfolio is positioned in such a way that lower interest rates and/or a risk off market will provide support to the underlying companies. We view it as the more conservative of the strategies we run.

AnComp*

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Industrials | BAE Systems | United Health | Health Care |

Insurance | Prudential Plc | London Stock Exchange | Financials |

Insurance | Aviva Plc | Equinix | Real Estate |

Technology | Broadcom | PepsiCo | Consumer Staple |

Health Care | HCA Healthcare | Compass Group | Consumer Discretionary |

*YTD performance |

High Quality/Diversified

The AnBro World’s Biggest Brands Portfolio (JSE: BRNDZ) ended the quarter up 8.81%. The year-to-date tally has moved to a gain of 15.5%. The large cap big tech weights in this portfolio drove its performance and subsequent recovery in the second quarter. This is considered a high quality, diversified, global portfolio by the team at AnBro. It is a thematic portfolio tracking consumer preferences on a worldwide basis and is ‘on trend’ for global consumption evolution. Top and Bottom performers YTD are as follows:

BRNDZ*

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Consumer Discretionary | Alibaba Group | Meituan | Consumer Discretionary |

Information Tech | Oracle Corp | United Health | Health Care |

Information Tech | Intel | UPS | Industrials |

Information Tech | Samsung | Accenture | Information Tech |

Industrials | UBER | Salesforce | Information Tech |

*YTD performance |

High Growth/Blue Sky

The AnBro Unicorn Growth portfolio (JSE: UNICRN) gained 5.82% over the quarter. The year-to-date return is 11.44%. Smaller cap growth stocks were quite volatile in the quarter but sprung into life after the Fed cut rates. The portfolio was up 4.4% in September alone. The AnBro Team see this portfolio as the one that offers the highest growth and blue-sky potential. It suits long-term investors looking to buy a piece of companies that offer massive long-term upside. It is by far the most ‘exciting’ portfolio we run and certainly the most volatile too. It earns its place in a diversified portfolio via its potential for life altering returns.

Unicorn*

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Consumer Staple | Celsius Holdings | The Trade Desk | Communication Services |

Information Tech | Unity Software | HubSpot | Information Tech |

Consumer Discretionary | DoorDash | Goosehead Insurance | Financials |

Industrials | L3 HarrisTech | Accenture | Information Tech |

Information Tech | CrowdStrike | Manhattan Associates | Information Tech |

*YTD performance |

Core Portfolio

The AnBro TITANS Core portfolio (JSE: TITANS) has just completed its first full quarter as a listed AMC on both the South African and Frankfurt markets. This blue-chip, high-quality portfolio has kept pace with the S&P 500 over the quarter, despite having only a fraction of the allocation to MAG7 stocks than the broader market has. Its return for the quarter was 7.6%. Stand out returns from top class companies across multiple sectors provided a risk adjusted return that was superior to that of the market too with its current Sharpe Ratio of 1.1 and Sortino Ratio of 2. YTD the return is 16.11%.

This core portfolio should be compared to the S&P500 from both a returns and risk perspective over the LONG TERM. Any investor that invests in, or has considered, an S&P500 tracker fund for their core holding but is worried about concentration risk, could do well by considering the TITANS portfolio instead.

TITANS**

Sector | Top 5 | Bottom 5 | Sector |

|---|---|---|---|

Industrials | General Electric | United Health | Health Care |

Industrials | UBER | Salesforce | Information Tech |

Industrials | RTX Corp | Equinix | Real Estate |

Utilities | Constellation Energy | Procter & Gamble | Consumer Staples |

Real Estate | Welltower | EOG Resources | Energy |

*YTD performance |

Onward

As we look to close out another eventual year, the next quarter ahead looks likely to bring more interesting and noteworthy economic and market events. Heading into October the US government is shutting down as Democrats objected to Republican funding plans before the start of the new fiscal year on 1 October 2025. Previous shutdowns have had a relatively benign impact on markets overall, however, as is always the case each situation is different, so we remain vigilant to all potential outcomes.

Have a great quarter ahead and for those clients in the Southern Hemisphere enjoy the summer months!

Tags

27Four AltFi Bankruptcy-remote Blockchain Capital Markets Capital Markets of the Future Commodity Markets Crypto Markets DeFi Financial Markets Fully backed stablecoin Global Markets Gold Investing Investment Liquidity management Mesh Mesh Mint mZAR Open to all Private Equity Regulation Secondary Market Smart Assets Stablecoin transparency Tokenisation Tokenised cash TradFi Yield-bearing stablecoin yZAR ZAR stablecoin

Want to stay in the know on upcoming events and seminars?

Newsletter Sign Up

For more press information, please contact:

Connie Bloem, Product owner of Mesh:

hello@meshtrade.co / +1 604 671 4515